About

VW FWD

Global Reach

Careers

Resources

Practice Areas

Attorneys

Staff Members

Contact Us

VW Blog

Vela Wood Law

About

VW FWD

Mission & Values

Global Reach

Careers

Resources

Practice Areas

Attorneys

Staff Members

Contact Us

News & Events

Podcasts

Instagram

LinkedIn

TikTok

Twitter

Facebook

Vela Wood Infographics

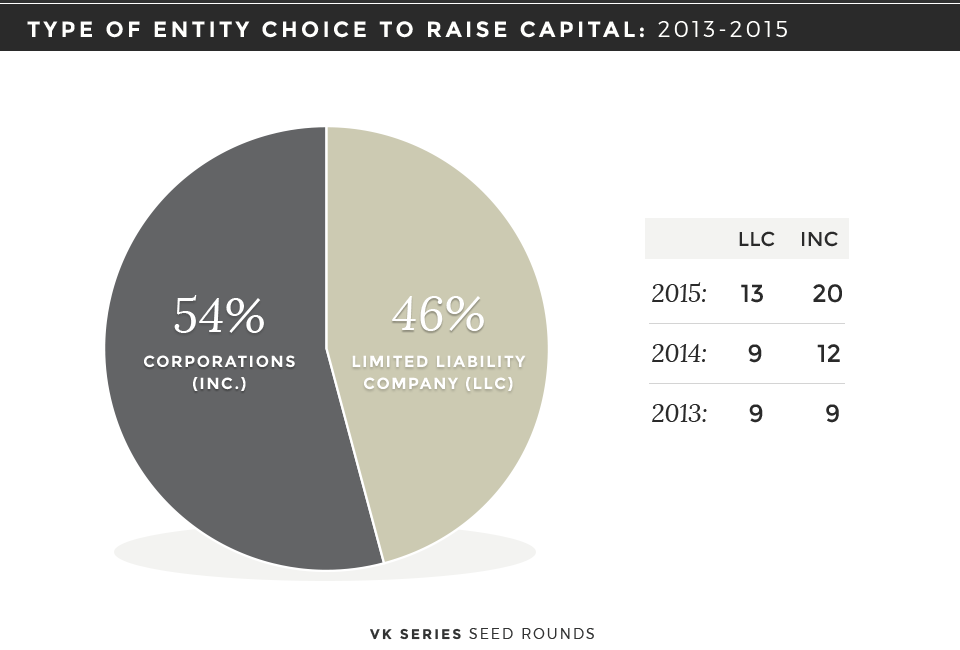

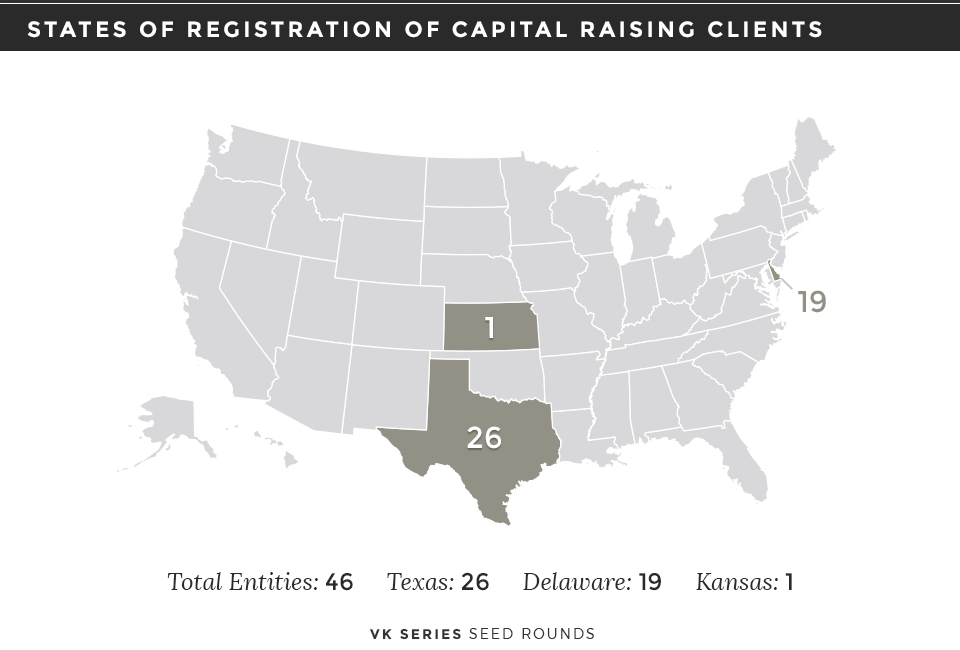

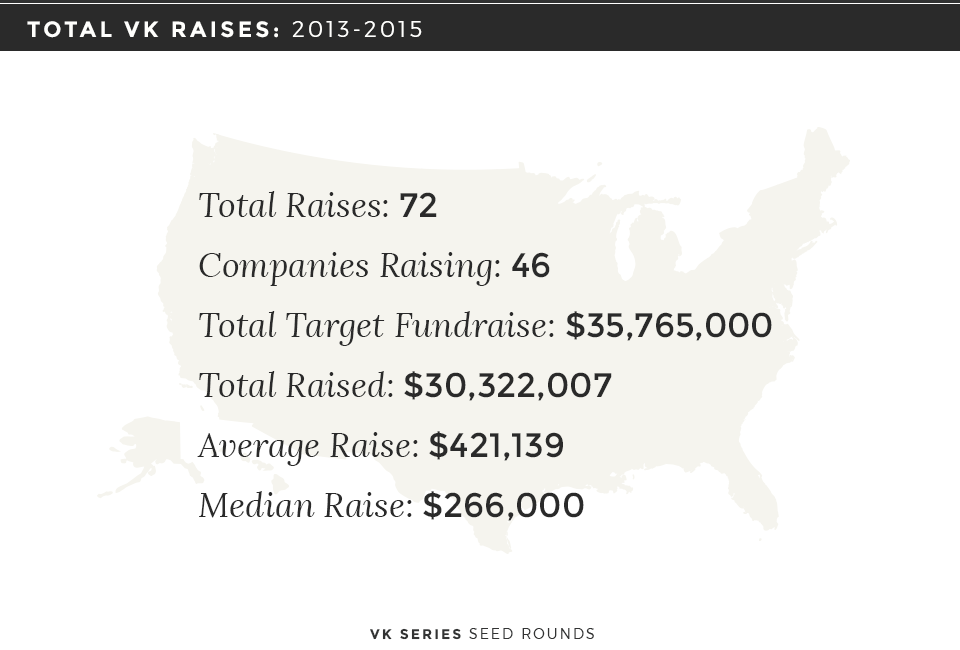

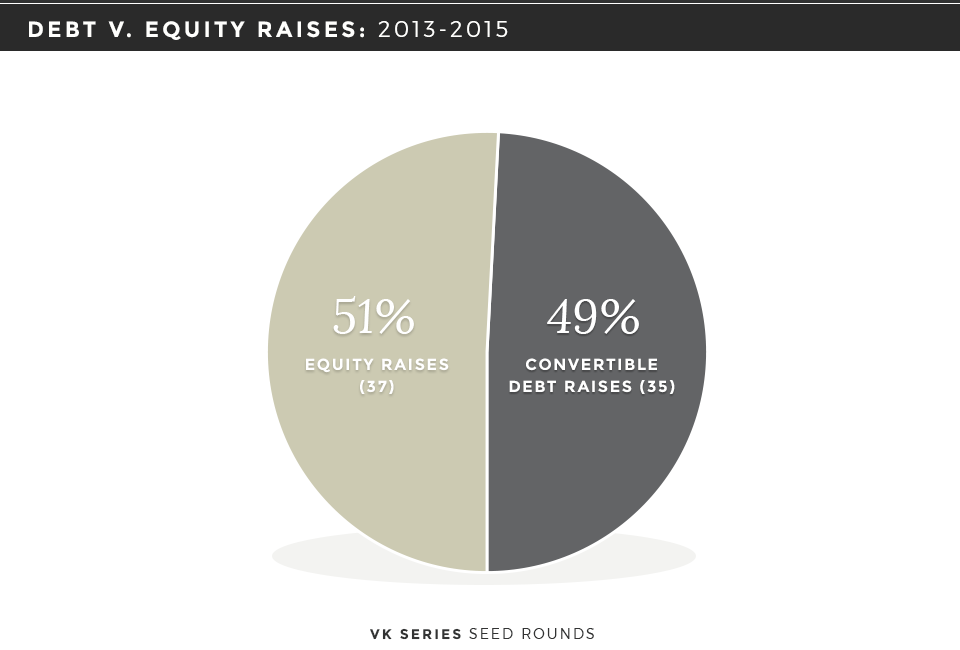

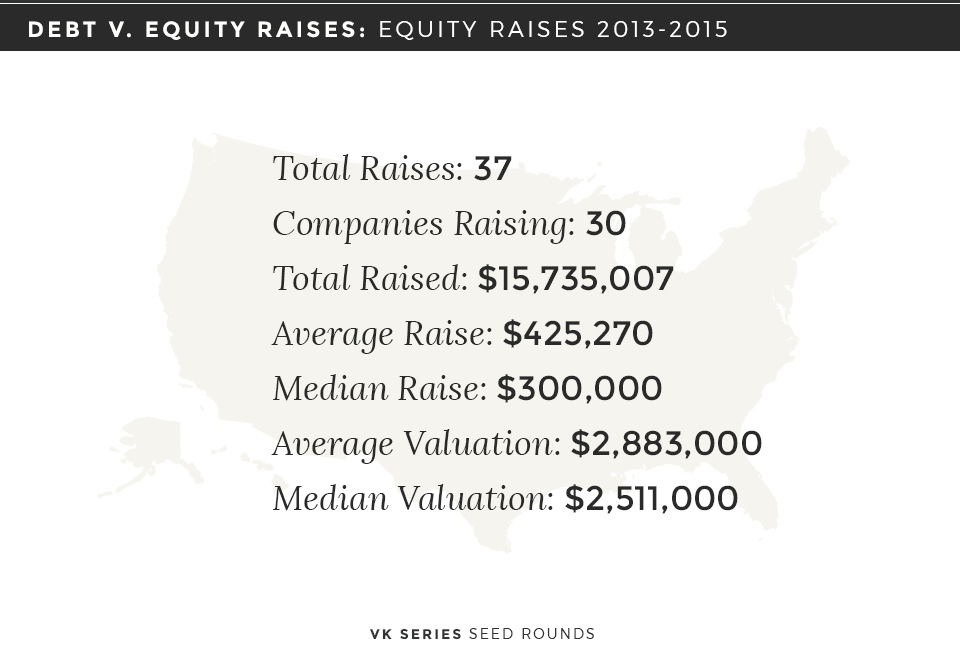

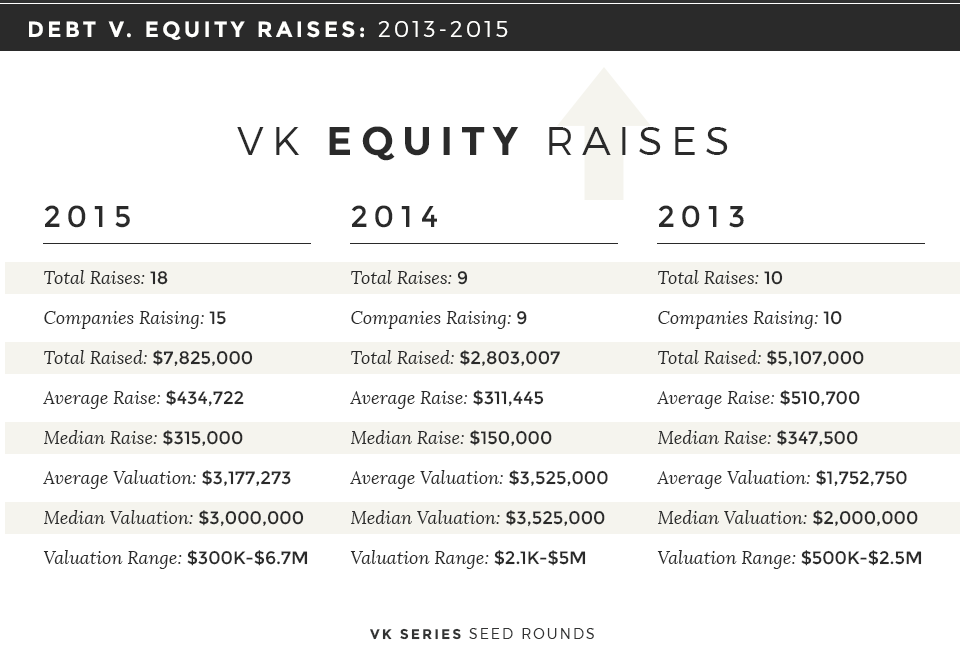

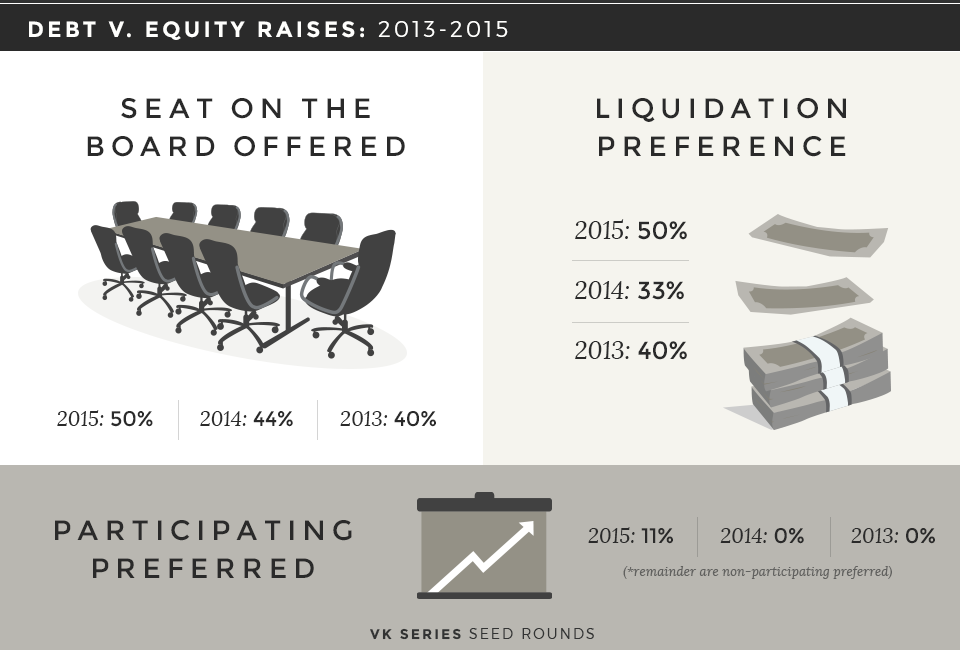

Venture Deals 2015: Seed Stage

See More Venture Deals

See All Infographics