The Unintended Consequences of Too Many New Venture Funds

By Kevin Vela

Venture capital activity is hotter than ever, which has led to more available capital and fueled the growth of many exciting companies. From 2020 to 2021, the aggregate deal value of VC investments in the U.S. increased from $167B to $330B.[1] In the same span, the number of deals increased from 12,173 to 17,054.[2] Increased deal activity is a great thing for startups and the venture ecosystem at large, but there are a host of consequences to understand. Much of the focus on these consequences centers on capital supply and valuations, but I want to focus on something else.

Micro-VC Funds and First-Time Managers

Though the data above measured all funding rounds and deal sizes across the VC landscape, the principal focus of this post involves micro-VCs and first-time managers. Based on what we’ve seen, their prevalence has brought along some unintended, and often overlooked, effects. The abundance of new funds and, as a result, new fund managers, has resulted in aggressive and off-market investor requests, typically through side letters, asking for:

- Board seats

- Perpetual pro rata rights

- Burdensome and perpetual information rights

- Wrong structure for the stage.

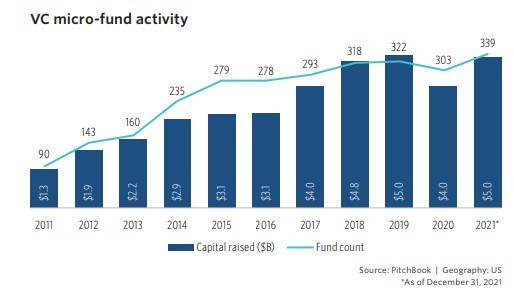

In 2021, 339 micro-VCs (often defined as funds under $50M in AUM) were raised, up almost 12% compared to the 303 raised in 2020. [3] At the same time, first-time funds accounted for approximately 40% of newly announced venture funds in Q2 2021.[4] A big jump from the 20% to 30% market share from the prior two years.[5]

This abundance of capital from the VC world has led to an uptick in early-stage valuations. Startups frequently, and often unknowingly, trade these higher valuations for more aggressive control rights. And because more micro-VCs and first-time managers are getting into the mix, we’re seeing more lead investors asking for investor-friendly terms in earlier and earlier rounds. As a founder, it can harm your company to undergo a Seed round when a convertible note round will do, or use Series A documents when Series Seed ones will do. As I’ve written before, rounds should be built with Lego Bricks: they are ubiquitous (region, country), they fit no matter the shape or color, and they are easy to stack on top of.

Of course, board seats, pro rata rights, and information rights are all normal asks. But when you have investors asking for (and receiving) such terms in the nascent stages of funding, you can wind up with too many cooks in the kitchen—and it can be to the detriment of everyone in the capital stack.

Why are these rights problematic?

Though it may seem so, investor rights should not be unlimited. At some point in time, the company needs to limit the number of cooks in the kitchen and, more importantly, limit its obligations to investors. Each of these rights come with their own set of concerns:

- Board Seats: We typically recommend a 2-1 board structure for our early-stage companies. In this structure, the Founders or other Key Employees make up the majority of the board, while the company offers up one board seat to its most significant investor. If a company starts filling up the board too early, such as in a Series Seed round, it can be difficult for the Founders to maintain control by Series B and later. Moreover, many new fund managers simply lack the experience, network, and resources to be truly impactful on a startup board.

- Pro Rata Rights: Pro rata is usually reserved for “Major Investors”—those who meet a predetermined ownership threshold. Issuing too many pro rata rights is a concern because each investor that exercises it translates to less investment opportunity for the next equity round’s new investors. On top of that, each pro rata right issued increases the administrative burden on the company due to notice obligations, and adds friction and delays to funding rounds.

- Information Rights: An information right is another right usually reserved for “Major Investors” that obligates the Company to deliver to the investor certain financial statements and other information about the Company’s operations. While it’s best practice to be transparent with all of your investors, Founders must consider that certain information deserves limited access. If you have a couple dozen shareholders with access to all of your financial information, a significant amount of your management’s resources may be spent explaining and justifying every single line item—a situation that will almost always be a net-detriment to your shareholders.

Example

Since we’re headquartered in Dallas we’re routinely on the other side of Mark Cuban and his team. I still remember how Mark and his team handled a board right as a Seed investor in one of the first deals we worked on together. He negotiated for the right to a board seat, but he didn’t take it. Since then, I’ve been involved in a few other rounds where he’s done the same.

I’ve never asked him directly, but I’m pretty sure he does this for a few reasons. First of all, early-stage startups are still relatively amorphous that the founders need room to feel things out and shape the company. Mark invested mostly because of the founders, so it’s wise to let them do their thing. Secondly, a Board seat carries certain duties and obligations, and with that comes liability. Less board seats = less risk. Finally, he and his team just don’t have time to sit on the board of every portfolio company. But having a right to sit in if needed can be very powerful.

Conclusion

In summary, it’s important that Founders and their counsel take caution in issuing these significant rights too early in the company’s life cycle. Round construction, including ancillary terms like pro rata rights, anti-dilution, and board seats, is critical. Remember a startup is highly unlikely to exit after a Seed or A round, so let’s use Lego Bricks and make sure the rounds are built with the next one in mind.

We know this is a lot to digest and the nuances of venture transactions can be complicated. That is why it is critical to consult with an attorney who is comfortable handling these types of matters to be sure you get them right. Hopefully this post will help you understand a few (of the many) important rights that can affect how your company is set up for future funding.

[1] NVCA Q4 2021 PitchBook Venture Monitor, pg. 5 (link).

[2] NVCA Q4 2021 PitchBook Venture Monitor, pg. 5 (link).

[3] The Rise of the ‘Micro’ Venture Capital Fund (Apr. 8, 2022) (link).

[4] A Comeback of the First-Time Venture Fund? (Sept. 7, 2021) (link).

[5] A Comeback of the First-Time Venture Fund? (Sept. 7, 2021) (link).

About the Author(s)

Kevin Vela

Kevin is the managing partner at Vela Wood. He focuses his practice in the areas of venture financing, M&A, fund representation, and gaming law.

Learn More