Revesting for Founders – Vesting Duration

Revesting frequently enters the conversation when new capital comes into a company—particularly in connection with priced rounds. Investors may ask founders to extend or restart vesting to realign incentives and reduce retention risk.

What’s “market” on duration? Here’s what we found in a survey of our recent early-stage deals:

• 81% of founders revest over a 3–4 year period

• 14% negotiate down to 2 years

• 5% extend to 5 years

Questions to consider:

• Founders: Should vesting align with milestones instead of time?

• Funds: Is revesting a retention tool, a risk mitigator, or both?

• Lawyers: Which strategies and market data guide your negotiations?

Equity Vesting Playbook – Advisors

Advisors play a valuable role in supporting startups by providing strategic guidance, industry expertise, and critical connections. In exchange for their services, startups often grant non-qualified stock options (NQSOs).

Below, we highlight four key vesting terms:

• Vesting Duration: How long until the options are 100% vested

• Cliff vs. No Cliff: Percentage of options that included a cliff

• Cliff Length: Length of the initial cliff period

• Vesting Frequency: How often options vest

Vesting Schedules by Role – How Long is Standard?

Vesting aligns incentives between the company and its stakeholders. Without it, startups risk compensating short-term involvement, which can lead to misalignment, unintended dilution and a potential hurdle to future funding. By structuring vesting schedules thoughtfully, founders can ensure equity is earned, not just granted, and that those holding it remain motivated to see the company succeed.

Beyond the well-established 4-year vesting schedule for founders, we reviewed over 1,600 recent option grants to determine the most common vesting terms for all other service providers—including employees, advisors and directors. Here’s what we found:

• 89% of founders and employees vest over 4 years

• 82% of consultants/advisors vest over either 2 or 4 years

• 92% of independent directors vest over 2 or 4 years

Questions to consider:

• Founders: What vesting schedule will keep you aligned with investors and the team?

• Consultants/Advisors: Does the schedule match the actual timeline for delivering value?

Revesting for Founders – Percentage of Shares

Revesting frequently enters the conversation when new capital comes into a company—particularly in connection with priced rounds. Investors may ask founders to revest all or a portion of their vested shares to realign incentives and reduce retention risk. What’s “market” on the number of shares subject to revesting?

Here’s what we found in a survey of our recent early-stage deals:

• The majority of founders revest 75%-100% of their previously vested equity

• 32% revest half of their equity

• 14% negotiate this down to one-quarter Questions to consider:• Founders:

How much equity are you willing to be subject to revesting for a deal?

• Funds: How important is having a founder revest?

• Lawyers: What provisions do you put in to protect founder equity during revesting?

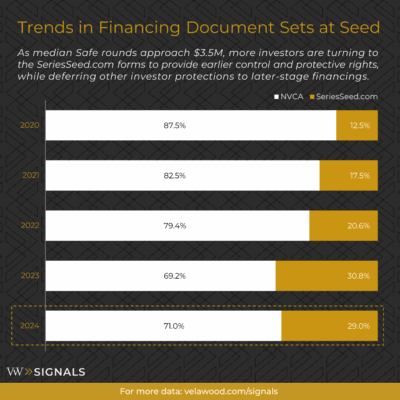

Trends in Financing Document Sets at Seed

What financing documents are companies preferring for initial priced rounds?

The NVCA model documents provide well-established, comprehensive investor protections and remain the standard for many financings. The growing adoption of SeriesSeed.com forms reflects a shift toward streamlined documentation that supports faster closings and lower upfront costs, while preserving flexibility to address additional terms and protections in later financings. Notable takeaways:

• SeriesSeed.com frequency more than doubled in the last five years

• NVCA remains the expectation, particularly in later-stage financings

Questions to consider:

• Founders: Are you prioritizing faster closings or long-term deal structure?

• Investors: Do lighter templates meet your expectations for early-stage protections?

• Counsel: Do you default to NVCA for consistency, or adjust based on deal dynamics?

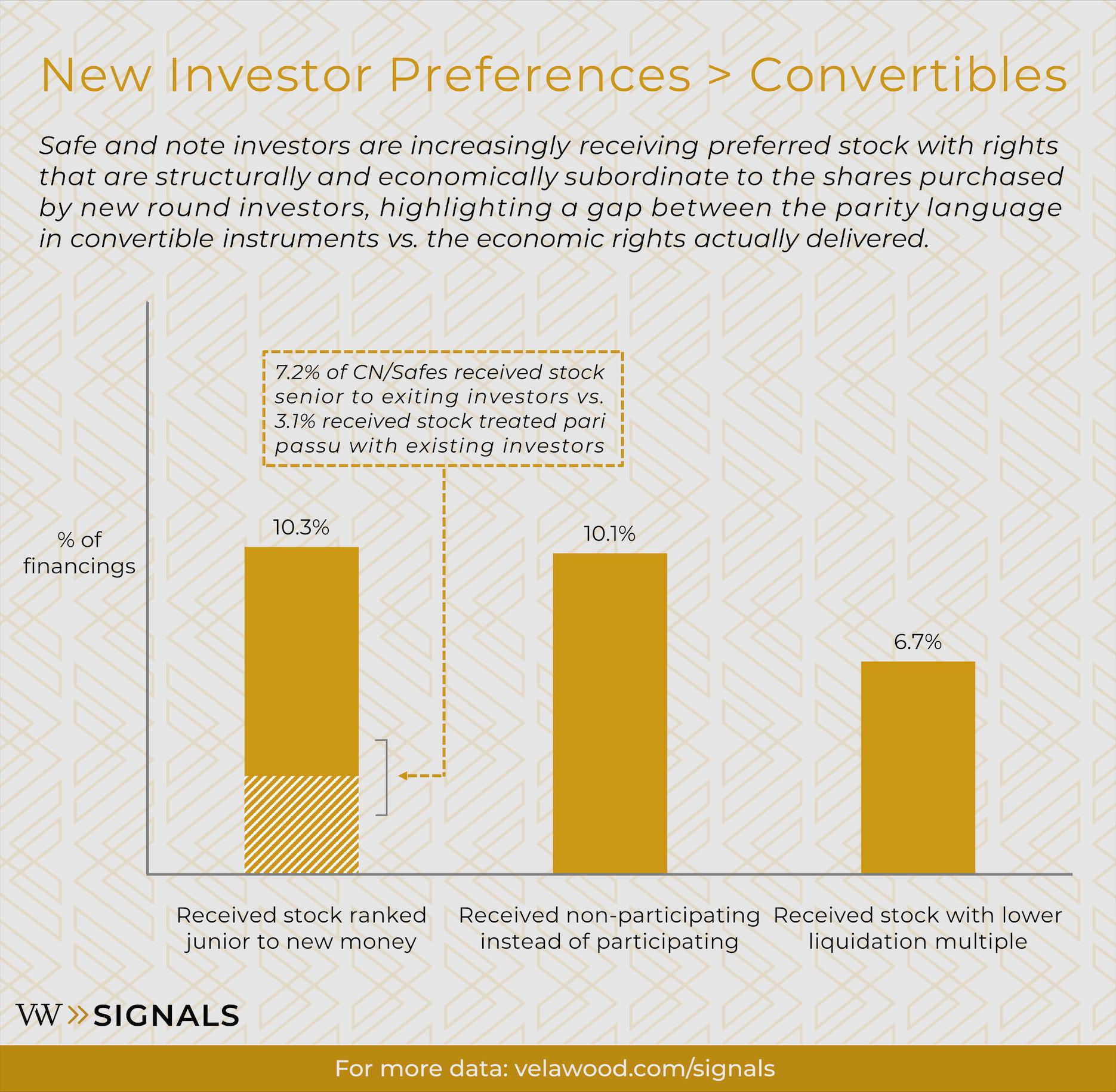

New Investor Terms Superior > Convertibles

How often do SAFEs and Notes convert into less favorable shares than those issued to new investors?

- 10.3% of rounds involved conversion into a junior liquidation class relative to new investors, including—

- 7.2% junior to new money but senior to prior preferred, yet

- 3.1% junior to new money and pari passu with prior preferred

- 10.1% received non-participating preferred while new money received participation rights

- 6.7% received a lower liquidation multiple than new investors

Why it matters:

Questions to consider:

- Founders: Does “same terms” still protect your earliest backers?

- Convertible Investors: Do you consider downside protections when signing SAFEs or Notes?

- Lead Investors: If you had to adjust one term for converting securities, would you choose priority, participation, or liquidation multiple?

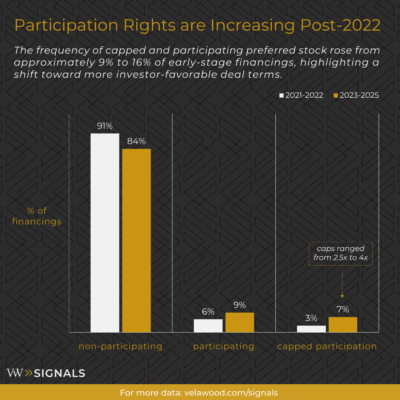

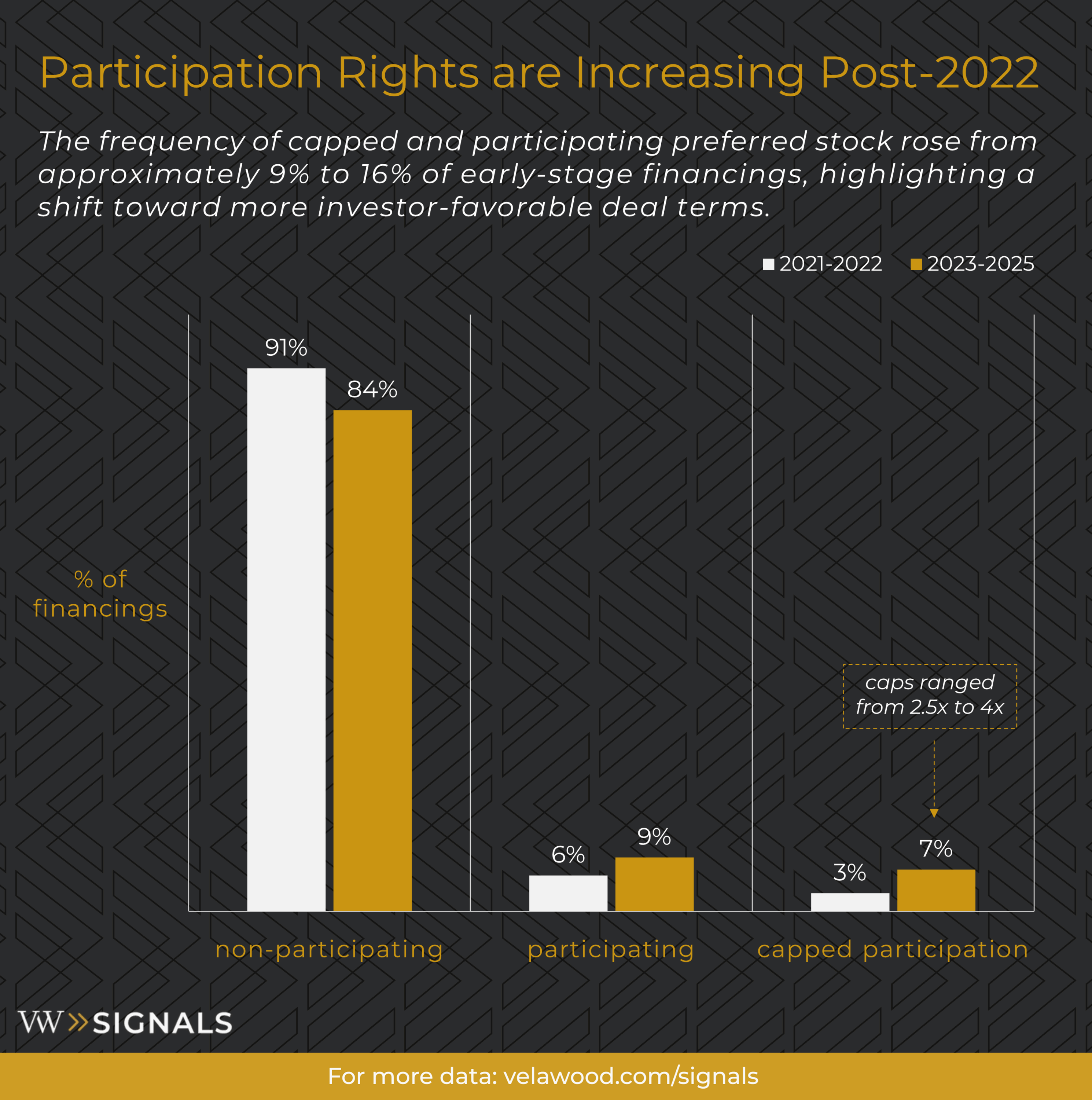

Participation Rights Are Increasing Post-2022

In addition to decreased valuations and less capital being deployed, what other market signals are forming?

We looked at our last 50 deals among companies with multiple equity financings and compared them to the height of the venture market in 2021-2022. We found that investors are negotiating for participation rights far more frequently – increasing from 9% to 16% since 2022. Where non-participating stock affects down and flatter exits for founders and investors lower in the capital stack, having investors with participating preferred stock affects exit outcomes across the board.

- Capped participation increased 57%

- Participating preferred increased 33%

- Non-participating stock remains the expectation

Questions to Consider:

- Founders: Are you willing to accept an investment with participation rights or would you look for alternate forms of capital?

- Investors: Would you trade a lower valuation for a participation rights?