Most published venture data often reflect only a portion of the market. These datasets are skewed toward the coasts, where reporting is more consistent and venture capital is more concentrated. That means early-stage trends from the middle of the country often go underreported or unnoticed.

VW Signals is Vela Wood’s answer to that gap. Based in Texas and deeply embedded in the early-stage ecosystem, we see the deals that don’t always make the headlines—especially at the Pre-Seed, Seed, and Series A stages. VW Signals highlights the patterns we’re seeing across our venture practice and aims to offer a clearer view into early-stage investing between the coasts.

Follow on LinkedIn

Notifications

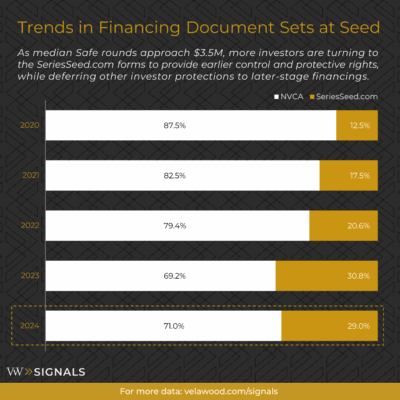

What financing documents are companies preferring for initial priced rounds?

The NVCA model documents provide well-established, comprehensive investor protections and remain the standard for many financings. The growing adoption of SeriesSeed.com forms reflects a shift toward streamlined documentation that supports faster closings and lower upfront costs, while preserving flexibility to address additional terms and protections in later financings. Notable takeaways:

• SeriesSeed.com frequency more than doubled in the last five years

• NVCA remains the expectation, particularly in later-stage financings

Questions to consider

• Founders: Are you prioritizing faster closings or long-term deal structure?

• Investors: Do lighter templates meet your expectations for early-stage protections?

• Counsel: Do you default to NVCA for consistency, or adjust based on deal dynamics?

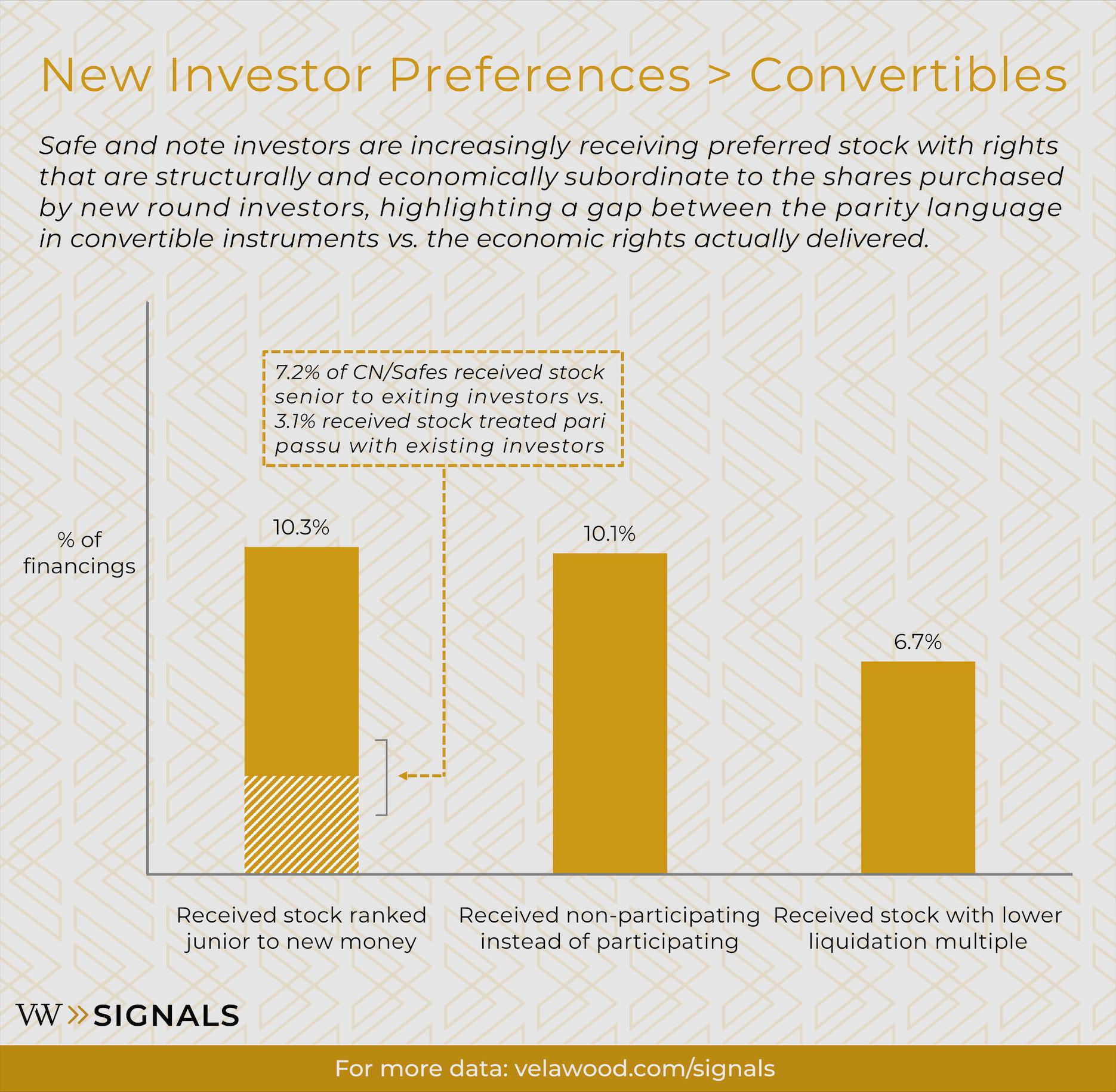

How often do SAFEs and Notes convert into less favorable shares than those issued to new investors?

Why it matters:

Questions to consider:

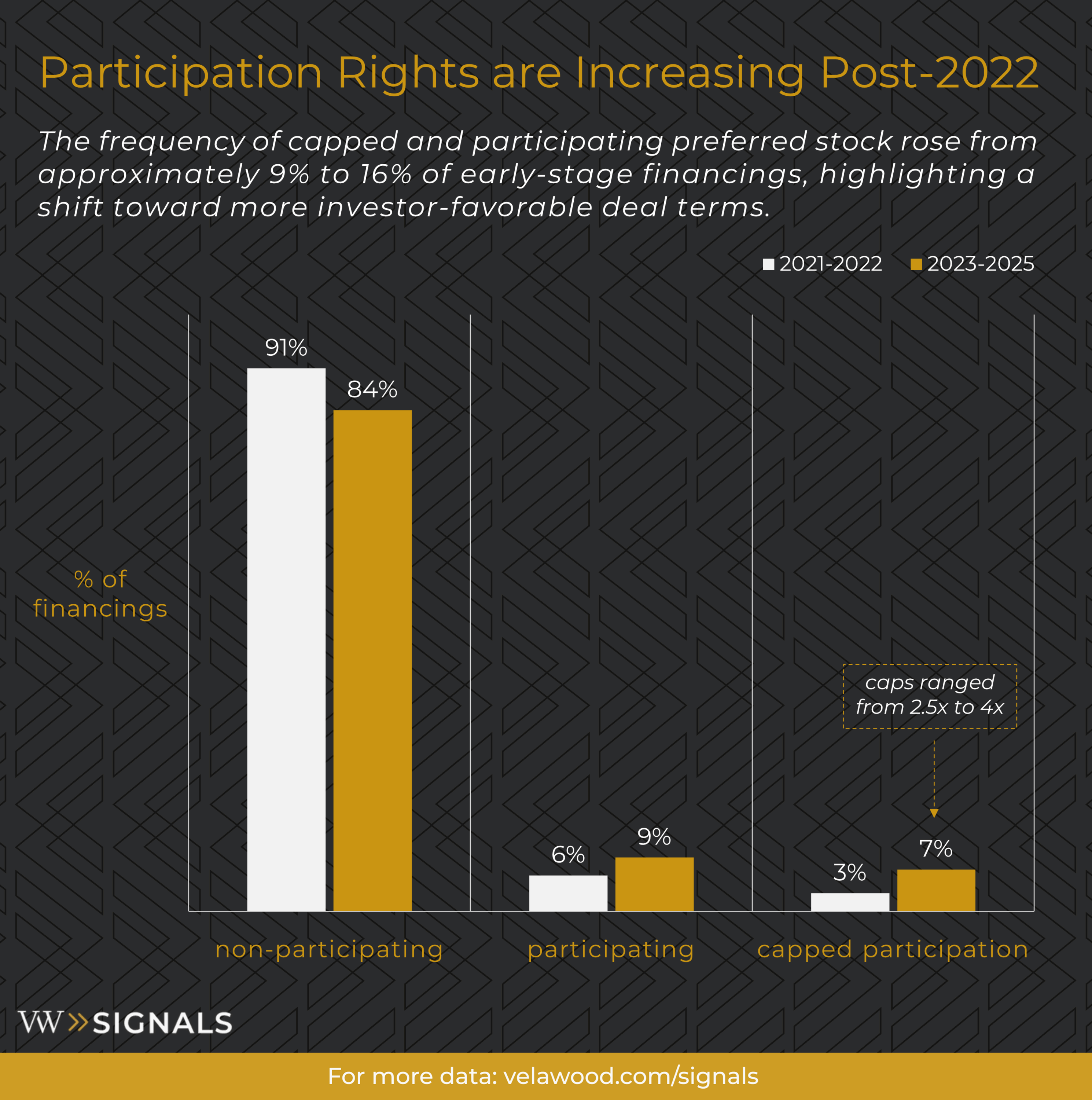

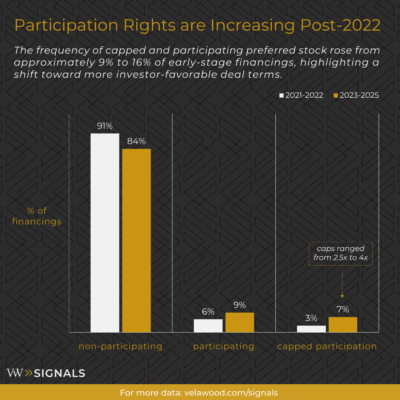

In addition to decreased valuations and less capital being deployed, what other market signals are forming?

We looked at our last 50 deals among companies with multiple equity financings and compared them to the height of the venture market in 2021-2022. We found that investors are negotiating for participation rights far more frequently – increasing from 9% to 16% since 2022. Where non-participating stock affects down and flatter exits for founders and investors lower in the capital stack, having investors with participating preferred stock affects exit outcomes across the board.

Questions to Consider: